Bitcoin is heading into one of the year’s largest options expirations at the worst possible moment.

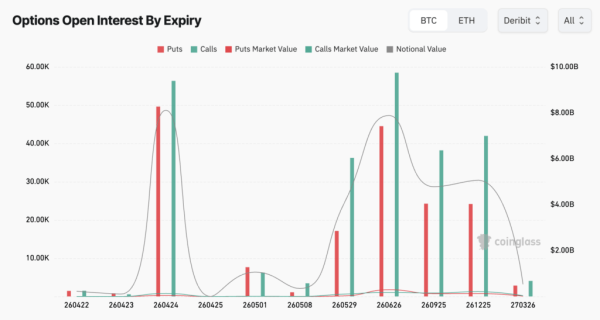

CoinGlass data shows roughly $8.07 billion in notional open interest for Deribit’s options expiring on April 24, split between 56,300 calls and 49,540 puts. While the ratio itself leans bullish, it’s sitting against one of the most uncertain macro backdrops in the past few months.

The expiry takes place three days before the Federal Reserve convenes for its April 28-29 meeting and four days before the Bureau of Economic Analysis publishes both Q1 GDP and March PCE inflation data on April 30.

That’s the densest macro calendar we’ve seen in a while, and it opens in an environment where Fed officials have spent the past week warning, on the record, that oil-driven inflation could keep borrowing costs elevated for considerably longer than markets had assumed.

There’s quite a bit of tension in the derivatives structure itself.

On Deribit, which now holds around $31 billion in total options open interest, surpassing even BlackRock’s IBIT, the April 24 contract has heavy call positioning, with around $395 million concentrated at the $75,000 strike. Max pain for the contract sits near $71,500 to $72,000, roughly $3,000 to $4,000 below the current Bitcoin price.

Chart showing the open interest for Bitcoin options on Deribit by expiry date on Apr. 21, 2026 (Source: CoinGlass)

Chart showing the open interest for Bitcoin options on Deribit by expiry date on Apr. 21, 2026 (Source: CoinGlass)

In options markets, max pain is the price level at which the greatest number of contracts expire worthless, which benefits sellers (in this case, large institutions and market makers) over buyers. That gap can create downward gravitational pull as settlement approaches.

The Fed has a new problem, and it comes from the Strait

The war that began in late February, when coordinated US and Israeli strikes on Iran triggered the closure of the Strait of Hormuz, the narrow waterway through which roughly 20% of global oil supply flows, sent Brent crude above $100 a barrel for the first time in years.

Iran’s reopening announcement on April 17 briefly reversed some of that pressure, with Brent falling roughly $10 to near $89 a barrel and Bitcoin surging toward the $77,000 to $78,000 range.

The relief, however, proved to be short-lived. On Sunday, the US seized an Iranian cargo ship bound for the Strait, seemingly unraveling the diplomatic progress from the end of last week, and Bitcoin opened Monday roughly 2.5% lower. The corridor remains more than 95% below pre-war levels in ship traffic, with major shipping firms still routing vessels around Africa because insurance companies won’t cover the passage, while military vessels remain active.

All of this is making everything the Fed does and says in the next few weeks so consequential, especially for Bitcoin.

St. Louis Fed President Alberto Musalem said last week that the oil shock is likely to keep underlying inflation near 3% for the rest of the year, nearly a full percentage point above the Fed’s 2% target.

This, explained, supports the case for holding rates in the current 3.50% to 3.75% range “for some time.”

New York Fed President John Williams essentially reiterated this, saying energy price increases are already passing through into airfares, groceries, fertilizer, and other consumer products, and that the process has “begun to play out already.” The CME FedWatch tool was pricing a 99.5% probability of a hold heading into the weekend.

The best summary of what’s at stake came from Fed Governor Christopher Waller in a speech on April 17, almost certainly the last substantive Fed communication before the pre-meeting blackout closes the window on fresh guidance.

Waller described the situation as a fork: a quick resolution to the conflict would allow inflation to keep moving toward 2%, preserving room for rate cuts later in the year. A prolonged conflict, on the other hand, would see higher inflation become embedded across a wide range of goods and services, with supply chain disruptions multiplying. The ceasefire is fragile enough that both paths remain genuinely live.

Why the Bitcoin options expiry is an amplifier

Large options expirations almost never drive prices cleanly in one direction, and the macro sensitivity that’s defined crypto markets since late February has made most crypto-native positioning signals less reliable than usual.

The more specific risk from Friday’s settlement is structural: a large expiry concentrated near the top of the recent range creates hedging dynamics among dealers that can amplify whatever macro signal arrives first.

If the Hormuz situation stabilizes and rate-cut probabilities tick up, the call-heavy positioning could translate into a squeeze through $75,000. If fresh escalation arrives, the same structure runs in reverse, with max pain near $72,000 acting as the level dealers work to defend.

Institutions spent much of this quarter selling upside Bitcoin exposure to generate yield, transferring risk to market makers. This created a structural cushion that disappears as soon as the contracts roll off, leaving Bitcoin more exposed to macro and geopolitical forces.

Waller’s April 17 speech was the last from a Fed policymaker before officials entered their pre-meeting blackout ahead of the April 28–29 gathering.

The FOMC decision will land without any guidance since mid-April, and markets will read it alongside Q1 GDP and PCE data that’ll capture, for the first time, what a Hormuz closure actually costs the US economy.

Bitcoin’s path through the next ten days runs through Friday’s expiry, a Fed decision, and a set of figures that could reprice the entire rates outlook. The derivatives market already has a position on the first event. We now have to see whether it holds through the other two.